How to Build a Subscription Telehealth App With HIPAA-Compliant Billing (not Stripe)

A D2C telehealth founder gets 3 weeks from launch. The app works. Patients book a visit and pay a monthly fee for their prescription. Billing runs on Stripe, because Stripe is the default every tutorial and every founder friend points to. Then Stripe's risk team flags the account and freezes payouts while they review the licensing. Recurring charges stop. Patients on a GLP-1 or an SSRI are a single billing failure away from a gap in their medication.

Founders learn this too late. Figuring out how to build a subscription telehealth app means making a billing architecture decision, and you make it on day one. You decide the processor, the data boundary, and the recurring logic early, or you'll pay for them later in frozen funds and disrupted care.

How do you build HIPAA-compliant billing for a subscription telehealth app?

Use a payment processor that signs a BAA and underwrites telehealth, like PaymentCloud for prescribing or Helcim for lower-risk clinical billing, since Stripe restricts the telemedicine category and signs no BAA. Build the patient portal, the data boundary, the Rx workflow, and the recurring-billing logic into the app, and let the processor touch only the card charge with no PHI in the record. Design the recurring billing as a care-continuity system, with smart retries and a protocol that separates a payment lapse from a patient's medication access.

Key Takeaways:

- Stripe is the wrong default for a prescribing telehealth subscription. It restricts the telemedicine category and signs no BAA, so prescribing apps need a BAA-signing processor like PaymentCloud or Helcim. Stripe stays fine for non-clinical wellness with no PHI in the transaction.

- Telehealth's high-risk classification is structural and assigned by the card networks. Prescribing maps to pharmaceutical merchant category codes, and card-not-present recurring billing puts you under VAMP and Mastercard chargeback thresholds. A high-risk merchant account is underwritten for that profile; a standard aggregator will freeze or terminate you.

- A failed recurring charge is a care-continuity problem, so design the billing logic like a clinical-safety system. A lapsed payment can interrupt a patient's medication mid-cycle. Build retries and a grace period into the flow, and keep a payment failure from automatically suspending clinical access.

- The boundary is the whole game: build the app and the billing logic, configure the processor for the card charge. Specode builds the patient portal, the data boundary, the Rx workflow, and the recurring-billing logic via its AI coder, while the processor only ever sees the card charge. Keep PHI out of the payment record entirely, starting with a generic statement descriptor and no clinical detail in the transaction.

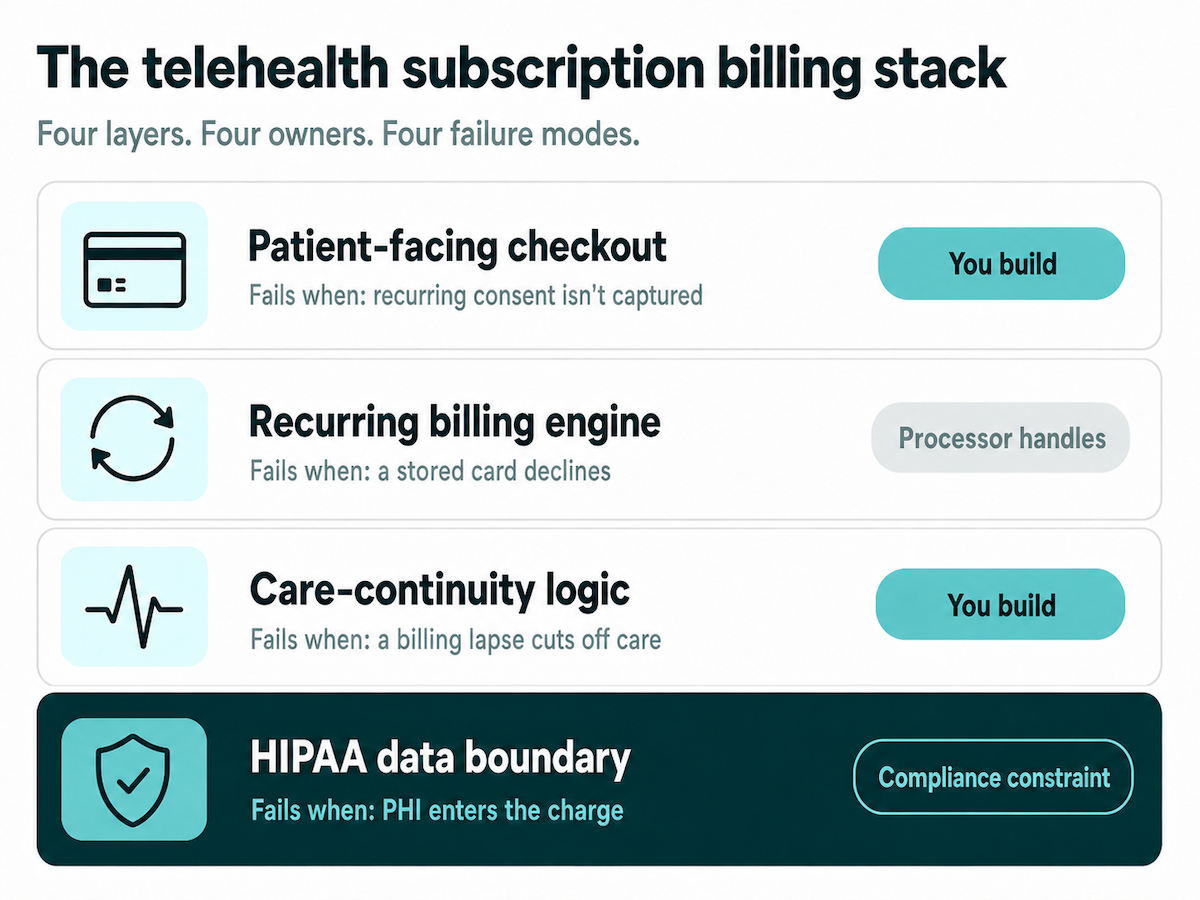

What a telehealth subscription billing stack actually needs

Most founders scope billing as one line on the build plan: pick a processor and drop in the SDK. For a telehealth subscription, that one line is doing 4 separate jobs.

- Patient-facing checkout. How the patient pays and consents to being billed on a schedule.

- Recurring billing engine. The stored credentials and the charges that run against them month after month.

- Care-continuity logic. What happens to a patient's clinical access when a charge doesn't go through.

- HIPAA data boundary. What the processor is allowed to see, and what it never should.

Each layer has a different owner and a different failure mode. Some you build, some the processor handles, some are compliance constraints you design around. Conflate them, treat the checkout as the whole stack, and you've made the Stripe mistake. Skip the care-continuity layer and you've built a patient-safety blind spot.

Pharmacy Times makes the point plainly: in healthcare, payment processing is now part of your compliance surface. That's why the data boundary belongs in the stack as its own layer, designed in from the start.

Why Stripe doesn't work for telehealth, and what does

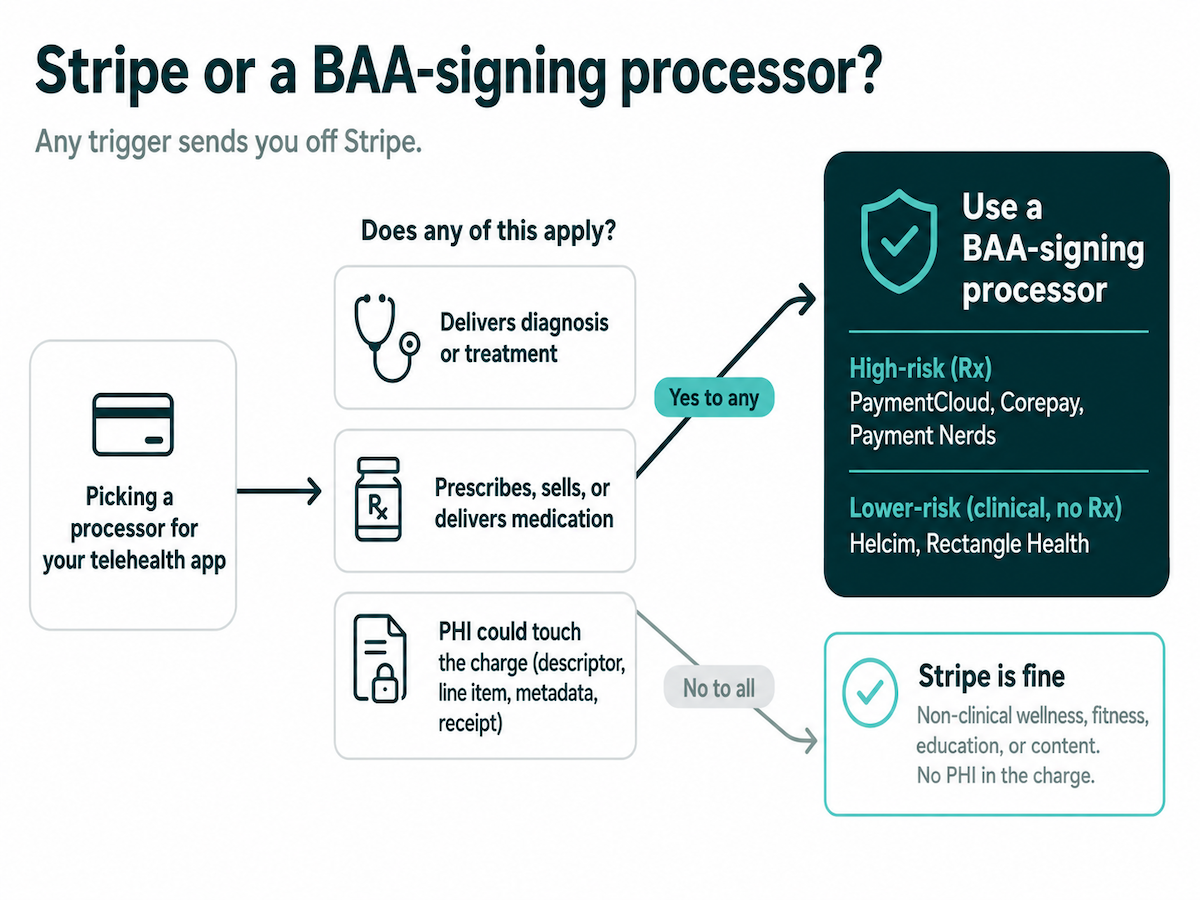

Stripe is the wrong default for a prescribing telehealth subscription, and it comes down to two gates: the category Stripe puts you in, and the BAA it won't sign. Plenty of founders search "is Stripe HIPAA compliant for telehealth" and walk away with a yes-or-no that misses both. Payment processing has its own carve-out under HIPAA, and that's exactly where the confusion starts.

The two gates Stripe puts in your way

Gate one is the category. Stripe files telemedicine under Restricted, so you can use it only with prior approval, granted case by case after you hand over license numbers and process docs. That approval is geographically limited and revocable at any time. Pharmacies are a "maybe," cleared in just 6 countries. Stripe even draws its own line: telemedicine means diagnosis or treatment by phone, text, email, or video, while wellness and education resources sit outside it.

Gate two is the BAA. HIPAA's §1179 exempts the bare card charge, so the payment itself usually creates no BAA obligation. Stripe signs none, because the providers underneath it won't either. So the moment PHI lands in the transaction, whether that's a clinical descriptor, a CPT line item, a diagnosis in metadata, or a clinical receipt, you're exposed. We go deeper on BAAs and gateways in HIPAA compliant payment processing.

The exception, non-clinical wellness with no PHI

Stripe is genuinely fine for one slice of the market: a subscription with no diagnosis, no treatment, no prescription, and no PHI in the transaction record. That covers real products:

- wellness and meditation apps

- fitness coaching

- nutrition and habit programs

- general health content

Keep Stripe if that's you. The line is clinical context entering the billing flow, and a meditation subscription never crosses it.

What does work, a BAA-signing processor that underwrites telehealth

A HIPAA compliant payment processor for telehealth does two things at once: it signs a BAA and underwrites the category. These processors come in two tiers.

- Lower-risk clinical billing. Helcim and Rectangle Health. Fine for permitted-category clinical billing with no prescribing component.

- High-risk prescribing specialists. PaymentCloud, Corepay, Payment Nerds. Built for Rx and subscription telehealth, usually running on the Authorize.net or NMI gateways.

PaymentCloud and Helcim are the two names to start with. Square is the one to flag: it publishes a BAA and works for permitted-category clinical billing, but its terms restrict telemedicine and bar online pharmacy, so it's out for prescribing.

The decision rule is simple. If your app delivers clinical care, or PHI touches the charge, you need a BAA-signing processor. Stripe is for the permitted slice only.

Why telehealth is high-risk, and what a high-risk merchant account buys you

Telehealth gets classified high-risk by the card networks, and the classification is structural. Founders read "high-risk" as a discretionary label and assume a clean chargeback record will talk an underwriter out of it. It won't. The pharmaceutical category and the monitoring rules put you there regardless.

Why the classification is structural

Prescribing telehealth maps to the pharmaceutical merchant category codes: MCC 5122 (drugs, drug proprietaries, druggist sundries) and 5912 (drug stores, pharmacies). Visa's April 2026 manual lists both among its card-absent high-integrity-risk categories. Add card-not-present recurring charges plus cross-state care, and that's what trips the label. The distinction matters: 5122 is wholesale Rx distribution and 5912 is retail pharmacy, so a prescribing telehealth app gets classified pharmaceutical even when it isn't literally coded 5122.

The monitoring math you have to live under

High-risk means living under chargeback monitoring. To see how VAMP affects telehealth billing, start with the thresholds, which run tighter than founders expect:

- Visa VAMP: the merchant Excessive threshold dropped to 1.5% on April 1, 2026, counting card-not-present transactions only.

- Mastercard: Excessive Chargeback Merchant at 100+ chargebacks and a 1.5% ratio, High Excessive at 300+ and 3%.

The VAMP telehealth math has a catch: fraud chargebacks count double, so you hit that 1.5% faster than the raw number suggests. Cross either line on a standard aggregator and the consequences land fast: fines, frozen funds, MATCH-list placement, and termination, each one a direct hit to patient care and payroll. For the Rx leg, card-not-present medication and pharmacy sales also need LegitScript certification (or equivalent) plus Mastercard registration. Consults alone don't.

What a high-risk merchant account buys you

A telehealth high-risk merchant account is underwritten for exactly this profile. It comes with dispute tooling and built-in tolerance for the chargeback ratios that would get you frozen or terminated on a standard aggregator. You can't change the classification, so you change the account that lives under it. Pick the account that matches the profile, and high-risk stops being a threat and becomes a line item.

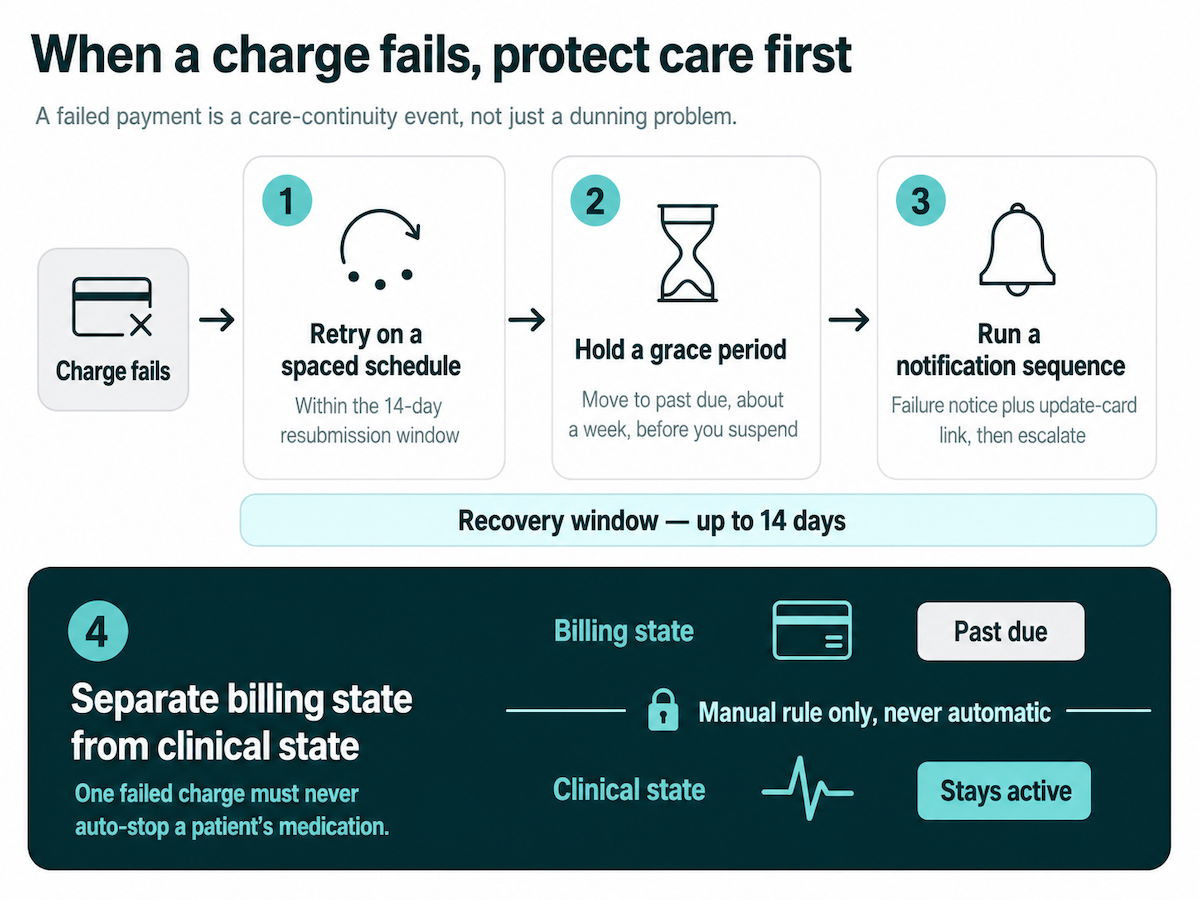

Recurring billing logic: handling failed payments without interrupting care

Most founders treat a failed recurring charge as a dunning problem: retry the card, move on. In a telehealth subscription, a failed charge can cut off a patient's medication mid-cycle, whether that's a GLP-1, an antidepressant, or a controlled substance. Pharmacy Times puts the stakes plainly: payment disruption interrupts medication fulfillment. That makes a failed payment a care continuity problem, and the billing logic that handles it a clinical-safety system.

The card-network rules you build around

Before you design anything, recurring billing for a healthcare app has to sit inside the card networks' stored-credential rules. Get express consent in an agreement separate from your general terms, capturing the last 4 digits, how the credential will be used, how you'll notify them of changes, and its expiration. The first charge is a cardholder-initiated transaction with strong authentication; every charge after that is a merchant-initiated transaction that references it.

A few more constraints shape the retry logic. On a declined recurring charge, the networks give you at least 14 days to resubmit when the decline reason code allows. For trials, store the card with a $0 account verification and send a reminder with a cancellation link at least 7 days before the first real charge. And run an account updater to refresh expired or reissued cards before they fail.

The failed-payment sequence that protects care

This is the part you actually build, and a CTO can hand it to an engineer as-is:

- Retry on a spaced schedule inside the network's resubmission window, which gives you the full 14 days to recover the charge.

- Hold a grace period. Move the subscription to a past-due state before you suspend anything. The length is your call, say a week; the networks don't dictate it.

- Run a notification sequence that opens with a failure notice and an update-card link, then escalates if the card stays dead.

- Separate billing state from clinical state. A care-continuity protocol keeps "payment lapsed" apart from "stop the medication," so a single failed charge never auto-cuts a patient's clinical access. A lapsed card is a billing event; turning it into a clinical one should be a rule you write deliberately.

All of this is logic you build, and the next section draws the line between what you build and what the processor handles.

What to build in Specode vs configure in your processor

Founders usually ask whether Specode does billing. The real work in subscription telehealth app development comes down to one boundary: what you build into the app, and what the processor handles. Draw that line right and PHI stays on your side of it.

What Specode builds vs what the processor handles

No billing component ships, and there's no billing skill. The recurring-billing logic is custom work the AI coder writes on your instruction. When it integrates your chosen BAA-signing processor, it asks for what it needs, like API keys and environment config, and does the integration itself. You're not wiring webhooks by hand.

Keep PHI out of the payment record

That last line, "only the card charge," has a concrete meaning. Keep PHI out of the payment record entirely:

- a generic statement descriptor like "SMITH MEDICAL PA," never "SMITH ONCOLOGY"

- no CPT codes or diagnosis line items in invoices

- no clinical metadata on the transaction

- no clinical detail in email receipts

- no medical reasons in refund notes

The processor sees a charge and a generic merchant name. Nothing about why.

Isolating the medication charge

There's one more move that keeps the riskiest charge off your books entirely: split the charge. You bill the clinical service through your processor, and a partner pharmacy bills the patient directly for the medication. In a GLP-1 program, you charge for the consult and the pharmacy charges separately for the semaglutide, so the prescription never touches your processor. If you're mapping this against a broader build, our D2C telehealth launch guide covers the rest of what subscription telehealth app development takes.

Get your billing architecture right from day one

Billing for a prescribing telehealth app is a day-one architecture decision. You build the HIPAA app, the data boundary, the Rx workflow, and the recurring-billing logic, then configure a BAA-signing processor for the card charge. That's the work Specode is built for: a HIPAA-ready foundation where the boundary between your app and the processor is drawn correctly from the first build.

If you already have a billing setup, run a Vibe Code Audit to check it against these rules and surface where PHI is leaking into the payment path. If you're starting from scratch, Vibe to Traction is where to begin. Either way, the goal is the same: a D2C telehealth billing stack you designed on day one and built to survive the card networks.

How do I prevent chargebacks in a telehealth subscription app? Use clear billing descriptors and an easy cancellation flow, lock in the stored-credential consent agreement, and add pre-dispute tooling like Compelling Evidence 3.0, RDR, and 3DS.

What is VAMP and how does it affect telehealth billing? VAMP is Visa's chargeback monitoring program. The merchant Excessive threshold dropped to 1.5% in April 2026, and recurring card-not-present telehealth billing is exposed. Exceeding it risks fines and termination.

Frequently asked questions

Not reliably for prescribing telehealth. Stripe restricts the category and signs no BAA, so Stripe HIPAA coverage ends at payment processing. Non-clinical wellness with no PHI is fine.

HIPAA compliant telehealth billing runs on a processor that signs a BAA and underwrites the category, like PaymentCloud for prescribing or Helcim for lower-risk billing.

It's structural. Prescribing maps to pharmaceutical merchant category codes (5122, 5912), and the card networks treat card-not-present recurring billing as high-risk. You can't argue out of it.

It can interrupt a patient's medication mid-cycle, a clinical and legal exposure. Design retries and a grace period, and keep a payment lapse from automatically suspending clinical access.

Use clear billing descriptors and an easy cancellation flow, lock in the stored-credential consent agreement, and add pre-dispute tooling like Compelling Evidence 3.0, RDR, and 3DS.

VAMP is Visa's chargeback monitoring program. The merchant Excessive threshold dropped to 1.5% in April 2026, and recurring card-not-present telehealth billing is exposed. Exceeding it risks fines and termination.